Oil Never Moves in a Straight Line: What History Tells Us

Every few years, the same debate resurfaces.

One side says:

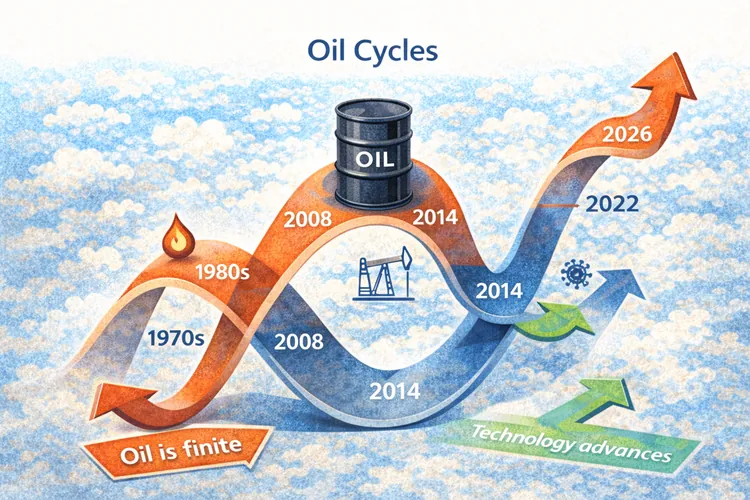

Oil is a finite resource. Reserves are shrinking. Prices must rise over time.

The other side argues:

Technology keeps advancing. Energy becomes more efficient. Alternatives expand. Oil will lose value.

Both positions sound logical.

Both have strong arguments.

But history tells a more complicated story.

Oil doesn’t move in a straight line upward or downward.

It moves in cycles.

The 1970s: Scarcity Shock

In the 1970s, oil prices surged after supply disruptions and geopolitical tensions.

For many observers, it seemed obvious:

global demand was rising, production was constrained, and oil would only become more expensive.

The “running out of oil” narrative gained momentum.

But that wasn’t the end of the story.

The 1980s: Collapse

High prices triggered new supply and efficiency.

- New oil fields were developed.

- Energy conservation improved.

- Alternative sources gained traction.

By the mid-1980s, oil prices collapsed.

The scarcity thesis didn’t disappear — but it was clearly not linear.

The 2000s: The Supercycle

Fast forward to the early 2000s.

Rapid growth in China and other emerging markets drove demand sharply higher.

By 2008, oil reached record highs near $140 per barrel.

Once again, many believed this time was different.

Emerging markets would fuel permanent upward pressure.

Then came:

- The global financial crisis.

- Demand contraction.

- And eventually, another structural shock.

2014: The Shale Revolution

U.S. shale production changed the supply landscape dramatically.

Technological innovation unlocked reserves once considered uneconomical.

Production surged.

Prices fell again — not because oil disappeared, but because supply expanded.

Technology, not scarcity, dominated the cycle.

2020–2022: Pandemic and War

The COVID-19 pandemic crushed demand in 2020.

Oil prices briefly turned negative in futures markets — something few models had predicted.

Then in 2022, geopolitical tensions and supply disruptions pushed prices sharply upward again.

The cycle turned once more.

So who is right?

Let’s revisit the two extreme views.

1️⃣ “Oil is finite, therefore prices must rise.”

Oil is indeed finite.

But price is not determined by physical depletion alone.

What matters is:

- accessible reserves,

- extraction cost,

- technology,

- substitution,

- demand patterns.

History shows that high prices stimulate:

- innovation,

- efficiency,

- and new supply.

Scarcity exists — but it doesn’t operate in a straight line.

2️⃣ “Technology will make oil obsolete, therefore prices must fall.”

Technological progress is real:

- electric vehicles,

- renewable energy,

- improved efficiency.

But global oil demand has proven resilient.

Emerging markets still depend heavily on hydrocarbons.

Transportation, aviation, petrochemicals — all remain oil-intensive.

History shows that technological change influences oil — but does not instantly eliminate it.

What cycles really show

Oil prices tend to move through recurring phases:

- Tight supply → price spike

- High prices → investment and innovation

- New supply or weaker demand → price decline

- Low prices → underinvestment

- Supply tightens again → repeat

This doesn’t mean prices are predictable.

But it does mean extremes rarely last forever.

Every time consensus becomes absolute — either about permanent scarcity or permanent decline — the cycle eventually shifts.

The cautious conclusion

Oil is not simply a story of depletion.

Nor is it simply a story of technological replacement.

It is a story of adaptation.

Markets respond.

Technology evolves.

Demand shifts.

Politics intervenes.

Historical cycles suggest one clear lesson:

Be skeptical of straight-line forecasts.

Because oil has rarely rewarded certainty — and often surprised both optimists and pessimists alike.