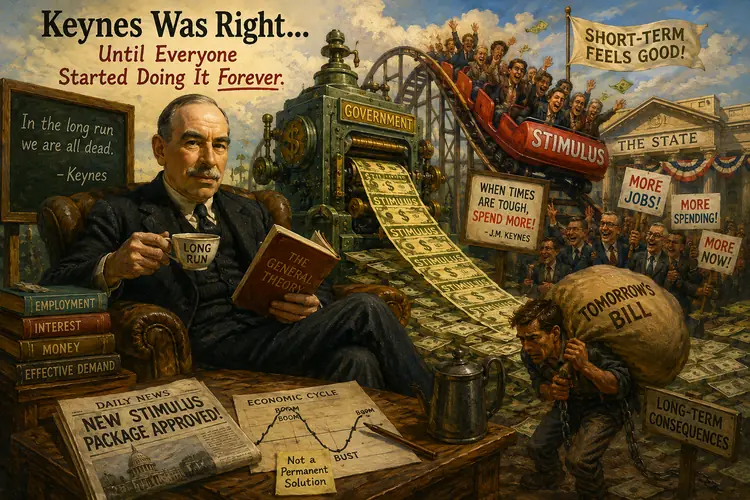

Keynes Was Right… Until Everyone Started Doing It Forever

The Economist Who Accidentally Changed Politics Forever

There are very few economists whose ideas escaped universities and entered everyday political life.

John Maynard Keynes was one of them.

Born in Britain in 1883, Keynes became one of the most influential economists of the 20th century during the turbulent decades surrounding the Great Depression of the 1930s and the Second World War. At a time when unemployment, bank failures, and economic panic were shaking much of the Western world, Keynes argued that governments should not simply stand aside and wait for markets to heal themselves.

That idea changed modern economics forever.

Before Keynes, governments often behaved like strict parents during economic crises:

- spending cuts

- balanced budgets

- austerity

- patience

- “the market will recover eventually”

The problem was that “eventually” can feel extremely long when millions of people are unemployed.

Then came the Great Depression. Factories stopped. Banks failed. Unemployment exploded. Entire economies appeared frozen.

And Keynes looked at the situation and essentially said: “Maybe this is not the moment for governments to sit quietly and wait.”

That idea changed modern economics forever. And perhaps more importantly, it changed modern politics forever.

The Radical Idea: Spend During Bad Times

Today, government stimulus feels almost normal. But in the 1930s, Keynesian thinking sounded revolutionary.

Keynes argued that during severe downturns, private demand collapses:

- businesses stop investing

- consumers stop spending

- fear spreads everywhere

And once fear becomes dominant, the economy can spiral downward on its own.

So Keynes proposed something unusual: if the private sector stops spending, the government should temporarily step in and spend instead. Not permanently. Not endlessly. Temporarily.

The government could:

- build roads

- fund infrastructure

- hire workers

- support large projects

- inject money into the economy

The idea was not to replace capitalism. The idea was to restart it. Like jump-starting a dead car battery.

This was the core insight: sometimes economies do not recover quickly by themselves because everyone becomes cautious at the same time.

And when everybody saves simultaneously, demand disappears.

Why Keynes Became Extremely Popular

Politicians quickly discovered something fascinating about Keynesian economics: people love stimulus.

Voters generally enjoy:

- government support

- infrastructure projects

- employment programs

- financial rescue packages

- lower unemployment

Businesses often enjoy them too. Markets definitely enjoy them.

And unlike austerity, stimulus feels emotionally optimistic.

Governments appear active. Responsive. Protective.

In many ways, Keynesianism transformed the image of the modern state. Governments were no longer expected merely to defend borders and collect taxes. Now they were expected to stabilize the entire economy itself.

That is an extraordinary expansion of responsibility. And once populations become accustomed to economic rescue, they begin expecting it during every serious downturn.

Keynes Probably Did Not Mean “Forever”

This is where things become awkward. Keynes argued for stimulus during crises.

Theoretically, governments would:

- spend more during recessions

- reduce deficits during stronger periods

- maintain long-term balance over time

That was the elegant part of the theory. The political reality turned out differently. Because stimulus is popular. Discipline is not.

Politicians discovered voters rarely celebrate:

- spending cuts

- reduced deficits

- fiscal restraint

But they absolutely celebrate:

- new programs

- tax cuts

- subsidies

- stimulus checks

- emergency support

So modern democracies gradually developed a strange habit: temporary intervention started becoming semi-permanent. Governments became much better at creating stimulus than removing it.

---

The Economy as a Patient on Policy Medication

Over time, many developed economies became increasingly dependent on government support.

A slowdown appears?

→ stimulus discussion begins.

Markets fall?

→ intervention expected.

Crisis somewhere?

→ spending package announced.

Economic weakness?

→ central bank support arrives.

This created a new kind of economic psychology. Modern economies increasingly resemble patients permanently attached to policy medication. And like all medication, stimulus can produce side effects.

At first, government spending feels powerful:

- jobs improve

- confidence returns

- demand increases

But repeated intervention creates dependency.

Businesses begin assuming support will arrive. Investors expect rescue. Governments normalize deficits.

And eventually economies stop functioning like fully independent systems. They begin functioning like systems constantly managed from above.

---

COVID Changed the Scale Completely

If Keynes opened the door, COVID kicked it off the hinges.

The pandemic produced one of the largest economic interventions in modern history.

Governments across the developed world spent astonishing sums:

- direct payments

- wage subsidies

- emergency business support

- expanded unemployment programs

- giant stimulus packages

In the United States alone, trillions of dollars moved through the system at incredible speed.

And for a while, the intervention appeared successful. Economic collapse was avoided. Markets recovered quickly. Consumers kept spending.

But the scale of the response changed something psychologically.

People realized governments could suddenly find enormous amounts of money whenever they considered something important enough.

For years, politicians argued endlessly over budget limitations. Then a crisis arrived. And suddenly the money appeared almost instantly. That realization permanently changed public expectations.

---

Debt Became Abstract

One of the most important side effects of modern Keynesian-style economics is psychological: debt stopped feeling real.

For decades, governments warned citizens about fiscal responsibility. Then developed nations began operating with debt levels that would once have seemed politically unimaginable.

The United States national debt climbed into the tens of trillions.

And yet daily life continued. Markets did not collapse overnight. Stores stayed open. Flights continued operating. Netflix still worked perfectly.

This created a strange new belief: perhaps debt simply does not matter anymore.

That is probably an overcorrection. Debt does matter.

But modern governments discovered they could sustain far larger deficits for far longer than older economic thinking assumed. Especially when:

- interest rates remain low

- central banks support bond markets

- investors still trust government institutions

The result is a financial world where enormous numbers increasingly feel abstract.

Trillion-dollar deficits barely shock anyone now. That alone would have sounded unbelievable decades ago.

The Political Addiction Nobody Admits

There is another reason governments love stimulus: it delays pain.

Almost every difficult economic decision becomes easier if financed through borrowing. Want new programs? Borrow. Want tax cuts? Borrow. Want military expansion? Borrow. Want infrastructure? Borrow. Want emergency relief? Borrow.

Debt allows politicians to deliver benefits today while shifting much of the cost into the future. Which works surprisingly well politically.

The future, unfortunately, does not vote yet. This is why modern politics often feels trapped inside permanent short-term thinking.

Stimulus solves immediate pressure. But long-term obligations quietly accumulate in the background.

And because each crisis justifies new intervention, the overall size of government involvement slowly expands over time. Not always dramatically. Sometimes almost invisibly.

The Inflation Reminder

For years, many economists argued massive spending and loose monetary policy would eventually create inflation. For a while, inflation remained surprisingly calm.

This encouraged a dangerous idea: perhaps governments had discovered unlimited economic flexibility.

Then inflation returned aggressively after the pandemic. And suddenly old economic rules started looking relevant again. Prices rose sharply across:

- housing

- food

- transportation

- energy

- insurance

Central banks then faced a painful dilemma. To slow inflation, they needed higher interest rates.

But higher rates also threaten:

- debt-heavy governments

- housing markets

- overleveraged companies

- fragile consumers

Modern economies had become deeply accustomed to cheap money and constant support. Removing that support suddenly felt dangerous.

The Quiet Transformation of Capitalism

Perhaps the biggest question surrounding modern Keynesian economics is philosophical.

At what point does a market economy stop being primarily market-driven?

Today, governments and central banks heavily influence:

- borrowing costs

- liquidity

- asset prices

- industrial policy

- crisis response

- labor markets

Private markets still exist. Competition still exists.

But the system increasingly operates with large stabilizing institutions constantly standing behind it.

Modern capitalism survived multiple crises partly because governments intervened aggressively.

But every intervention also slightly changed the character of the system itself.

The invisible hand now works closely with very visible government agencies.

Keynes Was Probably Right

This is the uncomfortable conclusion.

Keynes was probably right about crises.

Severe recessions can become socially and politically catastrophic if governments do absolutely nothing. The Great Depression demonstrated that clearly. Strategic government intervention can stabilize economies and reduce suffering.

The problem is not necessarily Keynesianism itself. The problem is that modern politics discovered stimulus is:

- useful

- popular

- emotionally reassuring

- politically addictive

And once societies become accustomed to constant economic support, removing it becomes extremely difficult. Temporary intervention slowly transforms into permanent expectation.

That is where modern economies now find themselves: somewhere between free markets and managed stability, between capitalism and continuous rescue operations.

And perhaps the strangest part is this: many people no longer even remember what a truly non-stimulated economy is supposed to feel like.