Gold Prices in the 21st Century — What They Really Reflect

Gold has a peculiar habit in markets:

It doesn’t move like a commodity.

It doesn’t behave like an industrial metal.

It doesn’t follow stocks or bonds perfectly.

Instead, gold prices reflect moods—not just money.

Understanding gold’s price history in the 21st century is not about predicting tomorrow’s level.

It’s about understanding why markets react to certain signals more than others.

A Quick Tour Through Recent History

Let’s look at the broad pattern.

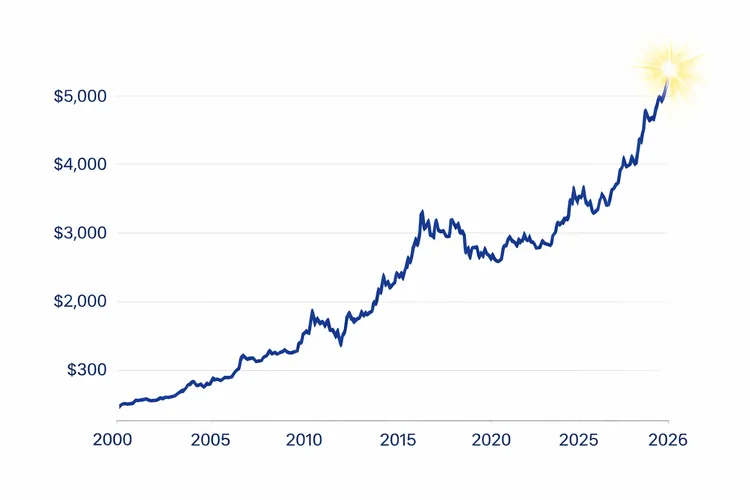

2000–2007: Quiet Accumulation

At the start of the millennium, gold was widely ignored by mainstream investors.

It wasn’t expensive, but it wasn’t cheap either.

During this period:

- global growth was steady

- equities were in focus

- bonds were tame

Gold drifted upward—but no one was watching.

This was the calm before the storm.

2008–2012: Crisis, Fear, and Safe Haven

The Global Financial Crisis changed everything.

As Lehman collapsed, credit markets froze, and banks teetered, gold became a symbol of safety.

In those years:

- gold prices rose dramatically

- investors flocked to assets perceived as “real”

- central banks began to buy more

Gold didn’t just appreciate.

It reflected fear.

The key insight here is simple:

When confidence in financial systems weakens, gold prices often rise—neither linearly nor predictably, but consistently.

2013–2019: Consolidation and Rotation

After the initial crisis wave, gold entered a multi-year pause:

- markets stabilized

- equities recovered

- technology stocks boomed

- yield-focused investing reasserted itself

Gold prices didn’t collapse, but they flattened.

That period shows us:

- gold doesn’t disappear when risk appetite returns

- it just takes a back seat

2020–2022: Pandemic, Policy, and Uncertainty

Then came COVID-19.

Unlike previous recessions, this crisis was:

- exogenous (not caused by financial imbalances)

- global and synchronous

- met with massive policy responses

Central banks cut rates to near zero.

Governments issued trillions in fiscal support.

Liquidity was everywhere.

Gold prices jumped again—not just because of fear, but because:

- real interest rates fell

- expectations of inflation rose

- bonds looked less attractive

In markets, gold often moves when real returns on alternatives are low.

2023–2025: Inflation, Rates, and New Equilibriums

In the mid-2020s, gold’s behavior has been shaped by a new dynamic:

- inflation spikes and then moderation

- interest rate volatility

- debates over monetary policy normalization

- geopolitical tensions

Gold doesn’t follow any one trend, but it responds to relative opportunity:

- when real yields are low or negative → gold rallies

- when yields rise and confidence in policy anchors strengthens → gold pauses

What Gold Prices Don’t Reflect

Gold prices are often misinterpreted as:

- a direct prediction of inflation

- a forecast of economic collapse

- a simple hedge against everything

In reality:

- gold does not rise every time inflation rises

- gold does not fall every time the economy recovers

- gold is sensitive to real interest rates and confidence dynamics, not nominal figures

A Simple Framework for Today

If you want to think about gold prices in the 21st century, remember this:

Gold reacts to three dominant forces:

1. Confidence in financial systems

When confidence weakens, gold often strengthens.

2. Real interest rates

Low or negative real rates reduce the opportunity cost of holding gold.

3. Geopolitical stress

Heightened uncertainty → higher demand for non-financial assets.

These are not perfect predictors, but they are consistent patterns, not random noise.

The Sixth Big Takeaway

Gold prices are not forecasts.

They are reflections of uncertainty, confidence, and relative opportunity.

Gold doesn’t tell us exactly what will happen next.

But it often tells us what investors are afraid of today.

In the final post, we’ll tie all of this together and ask:

Why gold still matters—not as money, but as a signal.